IPOs and the Mission to Mars

Happy Fri’Yay, dear readers! We are merely days away from the historic public listing of SpaceX stock so we thought it would be fun to discuss that and Initial-Public-Offerings (IPOs) in general, as this topic will dominate the financial zeitgeist for the remainder of 2026. After the SpaceX blast off, we will soon get offerings from additional private giants, Anthropic and OpenAI.

Before we get to the rocket science of it all, let’s not bury the lead: buying the most exciting stocks when they first go public is typically a terrible investment. WAIT, WHAT?! Yes, it’s true. THAT CAN’T BE TRUE!! We can prove it. FUN RUINER!! Been called worse.

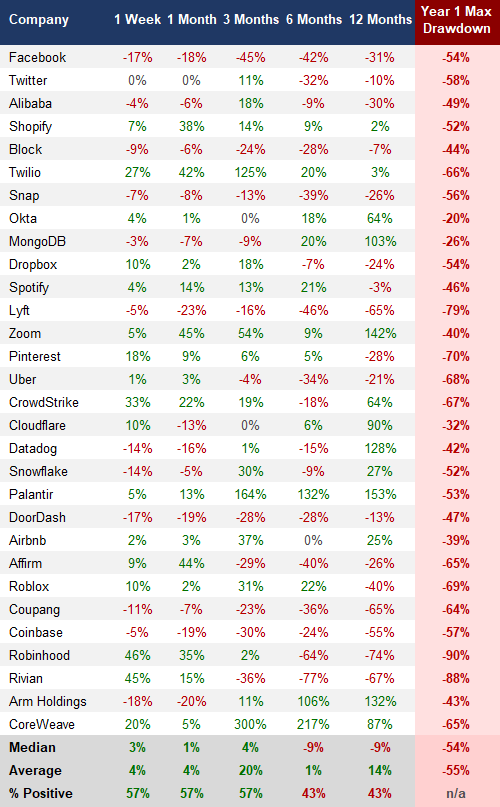

Below is a table of the largest and most prominent IPOs of the last two decades. You will see familiar and wildly successful companies like Facebook, Palantir, and Uber, but that’s not the point. Skip straight to the last column, “Year 1 Max Drawdown”, and behold the carnage. On average, these stocks dipped 55% at some point between the day they listed and the end of their first year as public stocks. Every single one could have been purchased after IPO at a MAJOR discount.

This table seems impossible, even for people in our business, because many of these companies eventually provided great returns, some even by the end of the first year, but it took time for the share prices to find their appropriate level lower (and for early buyers to get separated from their money). If we understand the IPO process a little better, this all starts to make sense.

Let’s try to clear up a misperception. When we think about a company going public, we often believe that this is the first time that the founders are offering the “privilege” to outsiders like us to invest. It was sort of like that in the past. If someone developed a widget or flying unicycle in their garage, they would get a few sales under their belt to prove the viability, then they would raise money by becoming a public stock to build out the operation and scale up – flying unicycles for all! In this case, early investors were buying a company in its infancy. They were risking their hard-earned capital to participate in the potential growth story of this new business.

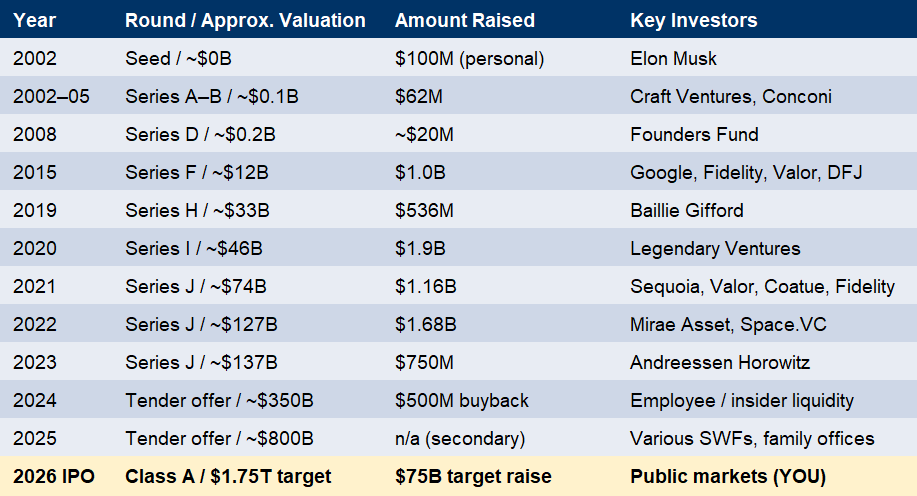

This is just not how it works these days. There’s a laundry list of reasons why but let’s skip that for now and use SpaceX as the proof for how different it is today. Below is the investor’s cap table for SpaceX that shows the years and amounts of money that the company has raised in the privat markets

SpaceX has raised approximately $11.9 billion in equity across 30+ private funding rounds since 2002. At a $1.75 trillion IPO valuation, the majority of the cap table holds stock at a cost basis of less than 5% of the offering price.

There are a couple major takeaways to consider – they have had investors for over 20 years and they have raised billions of dollars from millions of investors, including anyone who owns shares of Google (Alphabet). This isn’t a new opportunity for investors, it’s an opportunity for new investors to replace the current investors so they can realize their gains. Said differently, the entire purpose of the IPO is to get all of these people out of their ownership because they’ve had their money tied up for a long time, they’ve made massive gains and they want it back so they can buy something else.

If we think about the “old way” of going public with the flying unicycle example,

SpaceX would have gone public somewhere around 2006 or 2007. Instead, they were still raising money in the private market as recently as last fall. The conclusion here is that the bigger IPOs of the last couple of decades like Facebook, Uber, SpaceX or the upcoming Anthropic listing, are more like coronations or graduations. They are the mechanism for the company to thank and repay all of their investors by dumping shares of the stock on the public at the highest possible price they can get. In American business today, private companies stay private for way longer, raise crazy amounts of money and pick the absolute perfect timing to list. And it’s for these reasons that every stock on the table above saw its price go down significantly at some point in their first year of trading. As we continue this discussion, let’s get into a few SpaceX specific things. Sentiment around this IPO could be described as, “skeptical at best”, particularly from professional investors. Financial magazine, Barron’s, called it “Too Big to Succeed” a couple of weeks ago, stating that the true value of the company was probably half of the expected list price. We aren’t hearing a lot of big fund managers speak openly about interest in buying it for a couple of reasons. First, as we saw in the cap table above, many of us have had exposure to it for years via shares in Alphabet or even Bank of America. Second, let’s address this galactic elephant in the space room – the company’s market valuation.

SpaceX Valuation:

Just a quick reminder that when we discuss the value, the share price is a simple byproduct of the formula. The valuation that we truly care about is the total market cap of the company. The intentions is for it to be priced at $135 per share, while issuing 555.5 million shares to raise $75 Billion. That $75B represents 4.2% of the company which puts the total valuation at $1.75 Trillion.

For those scoring at home…

$135 x 555.5M =$74,992.5 B

$74,992.5B / 4.2% = $1,785,535 T

The numbers are so large that they’re hard to comprehend so here’s where it would sit by comparison:

NVIDIA (NVDA): $5.43T

Alphabet (GOOGL): $4.59T

Apple (AAPL): $4.50T

Microsoft (MSFT): $3.34T

Amazon (AMZN): $2.91T

Broadcom (AVGO): $1.98T

SPACEX (SPCX): $1.79T

Meta Platforms (META): $1.55T

At the IPO valuation, it would be the 7th largest company – almost two times the size of Walmart and Berkshire Hathaway. What jumps out when looking at SpaceX compared to these other stocks is that they make a TON of money…and SpaceX doesn’t. Here’s what estimated revenue looks like for these companies over the next year:

NVIDIA (NVDA): $375B

Alphabet (GOOGL): $440B

Apple (AAPL): $465B

Microsoft (MSFT): $300B

Amazon (AMZN): $730B

Broadcom (AVGO): $85B

SPACEX (SPCX): $13.5B

Meta Platforms (META): $235B

One last thing on valuation – and I’m sure some of you discerning readers caught it above in the investor’s cap table – when they raised money in December of 2025, the valuation was ~$800B or about 45% of the estimated list price just six months later. It’s more than doubled since December?

YOU TOLD ME SO:

Even if this note has been a slightly cool June rain on the IPO parade, get your phones out and ready on June 12th when SpaceX goes live because you can grab a screenshot of the price and dunk all over this article. Wall Street loves a good story you see, and having the largest IPO of all-time shoot higher when it opens trading is a lovely story. Put another way, the share price going down on day one is bad for business. As a collective, the investment banks bringing this listing public are set to make around $850M. That seems like sufficient motivation to make sure this thing gets off to a decent start.

Mechanically, this is done with all big IPOs by simply holding back shares and slowly trickling them out. That initial lack of availability will achieve the desired “pop” in the price so it won’t be a surprise to see shares moving up significantly from $135 to $150? $175? Who knows how much of a pop it will get, but we know, the way they see it is that if they don’t get an initial pop something went very wrong.

On Facebook’s first day of trading, it went from the offer price of $38 all the way up to $45 for what appeared to be a big win. Four months later, it was trading below $18.

YOU WILL OWN IT AND YOU WILL LIKE IT:

Regardless of whether or not we want to own SpaceX, we all are going to in some capacity. Another byproduct of private companies staying private longer and entering the public market with massive valuations is the effect on the indexes. The NASDAQ 100 and Russell 1000 indices have changed their rules for inclusion to fast track SpaceX in. They claim it’s too big to be left out (whatever that means). For now, the S&P 500 has declined to fast track them but they could still cave. Why that matters is that in this modern world of index investing, it will be harder to not have exposure to it. Like NVDA, GOOG, AAPL, MSFT, etc. it will be a prominent piece in all the big indices.

CONCLUSSION:

This trio of IPOs coming – SpaceX, Anthropic and OpenAI – is historic and fun to consider so this note could go on for days but let’s wrap it up with this. The three combined will need an estimated $250 BILLION of cash that is currently invested/sitting somewhere else. That’s a big number, even for Wall Street so it’s going to be very interesting to see how this first one goes in a week. These stocks certainly can be successful long-term, but it’s a big ask of global investors to find an extra $250B in the proverbial couch cushions. Given the history of prominent IPOs and the relative size of SpaceX, it will be no surprise to the author if shares can be purchased below the $135 offer price in the months to come. All the best.